Institutional-quality, private real estate investments used to be nearly impossible for the self-directed investor to access. Since the JOBS Act of 2012, and thanks to the advent of web-based investing platforms, professionally managed real estate and other alternative assets are now much more attainable for individuals seeking greater diversification. Meanwhile, a number of forward-looking self-directed IRA custodians have adopted more efficient processes, embraced technology, and prioritized integrating with the “platform investing” model.

What types of alternative investments can I access with a SDIRA?

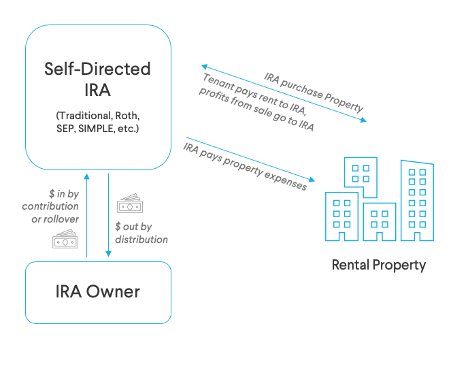

Self-directed IRA investors are legally permitted to invest in real estate, precious metals, hedge funds, or alternative assets. The only investment restrictions for IRAs are collectible items, life insurance, S-corporation stock, and prohibited party transaction (such as with family members). An IRA may leverage its investment with debt by using a nonrecourse loan to fund the balance of the investment. Online investment platforms that can accept self-directed IRA investments allow investors to passively invest in non-traded, alternative assets. Through EquityMultiple, for example, investors can access passive investments into debt, preferred equity, or equity positions in individual properties. This affords SDIRA investors a range of risk/return profiles and target hold periods.

When selecting real estate investments to allocate to via a SDIRA, many investors primarily consider their risk tolerance and time horizon with respect to retirement. Some SDIRA investors opt for payment priority — offered by debt or preferred equity investments — in advance of, or concurrent with, their target retirement date. Others seek longer-dated equity investments that will offer stabilized cash flow over a longer time horizon.

What are the best SDIRA custodians for passive real estate investing

Our more active investors typically choose a SDIRA custodian based on the following criteria:

● Fee structure

● Lack of red tape: how easy is it to obtain necessary approvals and fund investments?

● Tech integration: can the custodian interface with investing platforms to more efficiently complete investments and transfer funds?

There are a wide variety of fee structures among SDIRA custodians, so our investors will consider how frequently they plan on participating in EquityMultiple investment offerings and at what volume, seeking to minimize their aggregate transaction fee burden. The pros at Self Directed Retirement Plans, LLC can help you determine which custodian will be best given your investment objectives. Self Directed Retirement Plans LLC uses only “passive” custodians.

We also take the process a step further. We have been creating self directed IRA’s for over 15 years and ALL of our IRA clients benefit from “the next step. SDIRA’s are allowed to invest in LLC’s. We create underlying LLC’s for every SDIRA client. We structure the LLC’s as follows: they are manager managed LLC’s and our clients are the managers. The passive custodian is the member of the LLC FBO the IRA. We assist our IRA clients to establish a checking account in the name of the LLC. We then help our clients transfer all but $500 from the IRA account to the new LLC checking account. Our clients enjoy complete checkbook control, the passive custodian is truly passive and has no say on the day to day activities. This eliminates the above mentions aggregate transaction fees, asset based fees and saves time.The LLC basically has one purpose – to be the investment arm of the IRA.

How do investors use their SDIRA to invest in professionally managed R E investments such as EquityMultiple real estate offerings?

EquityMultiple facilitates investing in any of our investment offerings through a self-directed IRA: a custodian that allows real estate held in custody. With EquityMultiple and some other investing platforms, investors can rollover funds or fund this SDIRA directly. You will typically be required to instruct the custodian of your IRA to complete a written instruction, often known as a “buy direction” form attesting your (the beneficiary’s) intent to purchase an interest in this investment by the custodian (trust). The custodian will subsequently review the offering material or purchase agreement so that it doesn’t constitute a prohibited transaction. Lastly, the custodian countersigns the documents and wires proceed to the entity formed. Income, rental expenses, and sale from the asset are directed to the SDIRA and not directly to the beneficiary. The above is very true for most SDIRA’s. However, taking our “extra step” dramtically reduces the custodial expense and interference!

Tax Implications of SDIRA Real Estate Investing

A SDIRA account that invests passively in certain types of real estate asset can be subject to Unrelated Business Income Tax (UBIT). UBIT tax typically applies only when an IRA receives ordinary income as opposed to passive income from the investment held in custody. Passive income such as interest, rental income, dividends, or capital gain income is generally exempt and not subject to UBIT. There are two main instances where UBIT may apply:

If the real estate constitutes an income-producing business: UBIT tax is due if the real estate produces a service or product (for example a car wash, a hotel, or a restaurant.) If the intent was to sell immediately after purchase, then the investment can be subject to UBIT tax. Typically this timeframe is defined as less than one year.

Development: If the real estate activity is a ground-up development or a value-add investment that entails significant property improvements. In this case, a property that goes from land to structure and is sold will be required to pay UBIT tax.

When using the self-directed IRA in a transaction that will trigger the UBIT tax, the IRA is taxed at the trust tax of 10% – 37%. We encourage investors to consult with a tax advisor or IRA tax specialist to determine the tax implications of any particular real estate investment.

At Self Directed Retirement Plans LLC we also create self directed checkbook controlled 401 k plans. In fact we do 20 times more SD Plans the SDIRA’s. Ninety percent of our new clients wish to invest in RE using their retirement dollars. We ask two simple questions, Do you have any type of self employed income AND Do you have any fulltime employees. Self employed income can be consulting, Mary Kay, cleaning swimming pools etc. It is very easy to create self employed income.

We steer almost all IRA “callers” into SD 401 k clients. There are many reasons but a big difference is”. Real Estate investments using leverage (non recourse loans) in a SD 401 k DO NOT attract UBIT. This is absolutely HUGE. As stated above this eliminates the trust tax of 10% to 37%. When you combine using a ROTH sub account in the SD 401 K and leverage for R E investments you basically eliminate all taxes.

Rick Pendykoski is the owner of Self Directed Retirement Plans LLC, a retirement planning company based in Goodyear, AZ. He has over three decades of experience working with investments and retirement planning, and over the last ten years has turned his focus to self-directed ira accounts and alternative investments. If you need help and guidance with traditional or alternative investments, call him today (866) 639-0066.

In the wake of the latest economic crisis, there’s no such thing as true job security.With more than 10% of Americans unemployed, the last few months has seen a drastic fall in the employment rate. If you’re one of the millions of Americans, currently unemployed and wondering how to manage your finances, one question is likely to linger on: Should you keep saving for retirement when you no longer have a job?

How to decide whether to continue saving for retirement when unemployed?

It’s simple. Can you afford it?

If you do not have the money to pay your essential bills, such as housing, food, insurance, home and car repairs, debt payments, etc. saving for retirement should be the least of your worries. You need to use whatever money you have to cover these expenses.

If you do not have an emergency fund, at least six months of living expenses, you cannot afford to save for retirement. Emergencies can strike anytime, and if you have no money to cover it, you will be forced to sell investments, withdraw from your retirement account or borrow at a high-interest rate – and none of these options are good financial decisions when unemployed. So, focus on putting extra money toward your emergency fund instead of saving for retirement.

How to save for retirement when unemployed?

Get acquainted with IRAs

An individual retirement account (IRA) is a great option for people who do not have access to an employer-sponsored retirement plan such as a 401(k) account. In a traditional IRA, the contributions are deducted from whatever taxable income you have, much similar to a 401(k). However, in a Roth IRA, earnings are taxed upfront, but your withdrawals in retirement are not taxed. So if you’re not employed full-time, but have some earned income, IRAs can help save for retirement.

Rollover your old 401(k)

If you are unemployed, you will not be able to contribute to your employer-sponsored 401(k). However, the account is still yours, and the money in it is also yours. You have two options: let the money in your 401(k) lie as it is or roll it over to a traditional retirement account (IRA). Rolling over your 401(k) into an IRA could be a better option because you will have more flexibility and better investment options. And you can begin contributing to it once you start earning income.

Focus on optimizing your investment portfolio

If you no longer have a job, you may not be able to add to your retirement accounts, but you can definitely make sure that your portfolio is optimized. Make sure you have the right mix of investments and stocks in various asset classes and industries. Examine your investment portfolio to ensure that you are not under or over-invested in any area.

Consider reinvesting dividend income, if your finances allow

If you own dividend stocks, you may be tempted to redirect the dividend income towards paying your bills and get through the rough phase of unemployment. But if you can get by without doing it, consider redirecting your dividend income to buy more stocks and other investments. These small contributions to your retirement portfolio can add up to significant savings over time.

Focus on long-term growth, if you can

If you have some investments in a taxable brokerage account, you may be tempted to move them to dividend stocks or other income-generating investments for the extra income that you could use for covering your expenses. However, making this change can provide you the temporary relief, especially if you are unemployed, but it can harm you in the long run. Rather than making such adjustments in your portfolio, find some other sources of generating income or reduce your spending.

Losing your job after being gainfully employed for years can be a nasty shock. But the steps mentioned above can help you manage money and come out on the other side, financially stable and much in control of your life.

If you have recently lost your job, and need advice on the best way to manage retirement accounts at this time, call Rick at (866) 639-0066.

Rick Pendykoski is the owner of Self Directed Retirement Plans LLC, a retirement planning company based in Goodyear, AZ. He has over three decades of experience working with investments and retirement planning, and over the last ten years has turned his focus to self-directed ira accounts and alternative investments. If you need help and guidance with traditional or alternative investments, call him today (866) 639-0066.

Congress wants to force your heirs to take out your IRA within 10 years.

I want to give you at least 30 years. . . maybe even more.

Hi everyone, my name is Rick Pendykoski. For over 20 years I’ve been helping people learn the best ways to manage their retirement money. That is why when I read the latest tax law changes in the SECURE ACT. I was mad. Really mad.

Once again Congress has created a new law that forces people to overpay their taxes. Instead of incentivizing people to save money and build for their future, Congress wants to make sure they can tax your retirement plan within 5 or 10 years of your death.

That means those of you who planned on your family being able to stretch out the distribution of your retirement assets over their lifetimes, they are going to have to take much larger distributions each year. Because the distributions are going to be larger, the tax brackets are going to be higher as well. No one wins here except our do-nothing Congress!

Well, I have a secret for you. There is a way that you can use a trust to stretch out the payments for another 20 years at least. Now instead of your retirement money coming out in large clumps, just to be decimated by taxes, your kids can take over 30 years to spend down your earnings.

The Secure Act came into effect since January 1, 2020, and it includes significant provisions that will prevent older Americans from outliving their assets.

The new Secure act 2.0 has been passed by the house, not Senate or the “Prez”, to know more about it read our article Secure act 2.0 Other Changes!

How Will Secure Act Affect Your Retirement?

The Secure Act will inevitably affect many retirement account holders; the most immediate impact will be felt by those who have retired or nearing it. If you’re a saver or investor in your 50s or 60s, here are a few of the most significant provisions that you should be aware of:

1. Required Minimum Distribution Age Increased

Previously, 401(k) or IRA account holders had to withdraw required minimum distributions (RMD), when they turn age 70½.

With the implementation of the Secure Act, the RMD age has increased to age 72. However, this rule is only applicable to people who have not yet reached the age of 70½ by the end of 2019. People who already are 70½ years by the end of 2019 must withdraw their required minimum distributions this year; otherwise, they’ll attract a 50% penalty of their RMD.

2. Age limit for making Traditional IRA contributions eliminated

As life expectancies have increased, and more and more people continue employment beyond traditional retirement age, the Secure Act eliminates the maximum age for traditional IRA contributions. It also allows people of any age to continue contributing for as long as they are working (which previously prohibited people from contributing after they’ve reached age 70½, even if they were still working), thus enhancing their long-term retirement financial security.

3. Additional Roth IRA Planning Opportunities

With the increase in RMD age, the account holders have an additional two years to carry out Roth IRA conversions without worrying about the impact of required distributions. Converting to Roth allows the account holder to convert taxable money in an IRA into a Roth IRA by paying lower taxes than what they would be paying in the future.

4. “Stretch IRA” technique is eliminated

The term “Stretch IRA” describes a technique that a beneficiary uses to extend distributions from an inherited IRA over his or her lifetime. While stretch IRA allowed young beneficiaries to extend the payout over the decades, it also enabled them to spread out the payment of income taxes over a long period of time.

The Secure Act effectively eliminated stretch IRAs. For any deaths occurring after December 31, 2019, the beneficiaries must fully withdraw the funds from inherited IRAs within ten years of the account owner’s death.

However, the Act exempts certain kinds of beneficiaries from this rule: a surviving spouse, minor children, beneficiaries who are not more than ten years younger than the account owner, and those who are chronically ill and disabled. However, grandchildren of the account holder are not included among these exemptions.

5. Annuities as investment options in 401(k) plans

Considering the fact that Americans now live longer lives in retirement, annuities provide a guaranteed income over the course of a retiree’s lifetime.

The Secure Act allows more employers to provide annuities as investment options within 401(k) plans. Previously, the employer held the fiduciary responsibility to ensure the investment products are appropriate for employees’ portfolios, but under Secure Act, the responsibility of providing proper investment choices is now on the insurance companies, which sell annuities.

6. Encourages auto-enrollment

Auto-enrollment is effective in making people save more for their future. The Secure Act offers a tax credit to small employers (on top of the start-up credit they already receive) to offset the costs of auto-enrolling their workers into a 401(k) plan or SIMPLE IRA plan.

7. Easier for small businesses to form Multiple Employer Plans (MEPs)

Many small businesses are hesitant to offer a retirement plan to their employees because of compliance issues and high administrative costs. Multiple Employer Plan (MEP) allows small firms to collaborate and offer a retirement plan by sharing a plan administrator and administrative duties and reducing the costs. However, for businesses to join together, it requires them to have a common connection — for example, being in the same industry. So, many small businesses cannot collaborate with other businesses because of the lack of connection or similarity. With the Secure Act in effect, these rules are relaxed, making it easier for unrelated businesses to form an MEP.

8. Part-time workers can participate in 401(k) plans

Previously, employers excluded part-time employees from participating in 401(k) plans. But now, under the new rule, people who have been working for the employer for three consecutive years investing at least 500 hours or worked for at least 1,000 hours in one year is eligible to participate in retirement plans.

Rick Pendykoski is the owner of Self Directed Retirement Plans LLC, a retirement planning company based in Goodyear, AZ. He has over three decades of experience working with investments and retirement planning, and over the last ten years has turned his focus to self-directed ira accounts and alternative investments. If you need help and guidance with traditional or alternative investments, call him today (866) 639-0066.

There are different types of Individual Retirement Accounts (IRAs) that are designed to meet your needs. But all of them have one thing in common – they must have a custodian.

An IRA custodian is a financial institution that holds your account’s investments and ensures that all government and the IRS regulations are adhered to all times.

It’s not difficult to find IRA custodians, but the best custodian for you will depend on what type of IRA you want and what sorts of investments you want to make with it.

Traditional IRAs vs. Roth IRAs

The main types of IRAs that most individual investors set up are the traditional IRA and the Roth IRA. However, there is one basic difference between the two. A traditional IRA is a tax-deferred account. This means your contributions are tax-deferred until you start withdrawing your funds at retirement. With a Roth, your contributions are taxed. This means the money you withdraw from your account at retirement is tax-free. Additionally, both traditional IRA and Roth IRA allow your money to grow free of income tax.

Self-Directed IRAs

WithtraditionalorRoth IRA, you can have your account self-directed or managed through a custodian. In aself-directed IRA, you have the freedom to choose the funding methods and a wide variety of investment instruments. The custodian allows you to make investments outside the traditional world of investments including bonds, stocks, exchange-traded funds, and mutual funds.

Types of Custodians for Standard IRAs

If you choose to go with a non-self-directed IRA, there are a number of different financial institutions that can serve as custodians, once you’ve set up your account with them.

Banks: If you want to invest in money market funds or FDIC-insured security of CDs, the bank can be a good option. However, banks generally do not offer many investment choices outside the traditional ones. Some banks offer broker-types services, but they charge a high fee, probably higher than the brokerage.

Brokerage Firms: If you want to invest in individual bonds, stocks, mutual funds, or ETFs, you can opt for brokerage firms to be your IRA entity.

Mutual Fund Companies: Mutual fund firms also offer their ETFs and mutual funds for you to invest in.

Insurance Companies: Insurance companies offer their flexible premium annuities as basic IRAs. These annuities offer automatic account management, account value protection, and death benefit options. They are either variable or fixed. That said, IRAs are already tax-advantaged accounts. Insurance companies offering tax advantages of annuities is redundant. Additionally, you may have to pay high fees for having these annuities.

Robo-Advisors: Robo-advisors are relatively new online investment platforms that offer algorithm-based portfolio management advice. These platforms are automated. This means there is no human intervention. Hence, the fees and other expenses are low.

Custodians for the Self-Directed: If you want to choose a self-directed IRA, it can be a little complex. For a self-directed IRA, there are three types of providers: custodians, administrators, and facilitators. However, only the custodians have direct approval from the IRS and are authorized to hold assets.

The other two, administrators and facilitators, are actually intermediaries between you and your custodian (the one that holds your assets). Therefore, if you want to go ahead with a self-directed IRA, it’s better to stick to a true custodian.

All the institutions mentioned above can theoretically serve as custodians for your self-directed IRAs. But if you are leaning towards making non-traditional investments that are open to your self-directed IRA, you need to be particularly careful about your choice of custodian. If you are not careful, you can easily violate the IRS rules and pay severe penalties.

Tips for Choosing IRA custodian

Your chosen IRA custodian can either be an IRS-approved, non-financial firm or a financial institution given IRS approval. And if you are choosing a bank for setting up your IRA account, then the bank becomes your IRA custodian. The same stands true if you invest in a certain mutual fund family. Using such IRA custodians will save you a lot of money as their fees are relatively lower in comparison to institutional accounts. But, if you are choosing IRA custodian for a self-directed account, then make sure you choose an IRA custodian keeping the following 5 factors in mind.

A Wide Range of Investment Options The bigger the assortment of alternate investments, the more options you have to diversify your funds. So if you want to invest beyond stocks, bonds, ETFs and mutual funds, then your chosen IRA custodian should be able to help you look for non-traditional options like real estate and privately held companies.

Low Maintenance Fees Fees come in various forms – annual maintenance fees, commissions for making trade, loads for mutual funds and the like. So, if your chosen IRA custodian charges a certain type of fee, check if it is uniform across custodians because these fees are not a “given”. And if you are investing in mutual funds, make sure your custodian offers different types of no-load mutual funds.

Knowledgeable About the Rules If you have multiple IRA accounts then according to experts, you should consolidate your accounts into one fund and delegate a single IRA custodian. Your IRA custodian should be knowledgeable about the rules of the IRS, the rules based in tax law, and also know which types of IRA accounts cannot be consolidated.

No Restrictions on Investments Certain IRA custodians limit your investment options because the nature of their charter is restricted. These limitations may not be the same as the restrictions imposed by the IRS. So, make sure you choose an IRA custodian with no restrictions. When you are opening an IRA account, make sure your choice is based on the type of account you prefer – Traditional or Roth. If you want to diversify your portfolio then a self-directed IRA will give you the freedom to take check book control of your finances.

Prompt Services Unless you are fine working with a robot advisor, easy access to a knowledgeable and experienced financial advisor is very important. When you are managing a self-directed IRA, a vague or incomplete answer is the last thing you’d want to deal with.

Call Self Directed Retirement Plans LLC at (866) 639-0066 today to learn more about the alternate investment choices you can make with a self-directed IRA.

Rick Pendykoski is the owner of Self Directed Retirement Plans LLC, a retirement planning company based in Goodyear, AZ. He has over three decades of experience working with investments and retirement planning, and over the last ten years has turned his focus to self-directed ira accounts and alternative investments. If you need help and guidance with traditional or alternative investments, call him today (866) 639-0066.

You may not be a millionaire, but you may have reached a stage in life that makes you think that you have done all you possibly can to have a blissful retirement.

You are fortunate that your retirement planning has accumulated more than you need. Probably you don’t need to rely on IRA or 401(k) plan; your pension and Social Security benefits are enough to sail you through your retirement smoothly.

So, because you don’t need the money held in IRA or401(k), it gets piled up. But IRS doesn’t want you to keep your money as it is in your retirement accounts. When you turn 70½, the Required Minimum Distribution (RDMs) kicks in. This means you have to withdraw a certain percentage from those tax-advantaged accounts each year, whether you want it or not. The worst part of it all – the percentage increases as you age.

And If you fail to withdraw the RMD, you may need to pay 50% of your Required Minimum Distribution amount each year as a penalty.

However, the issue is taxes. If you wish to gift your money to your child or your loved ones, you have to pay income taxes on what you withdraw, and also pay tax if you let the amount stay in the accounts as it is.

Here is how your IRA or 401(K) can become tax free gift for your loved one.

#1 Gift money after reviewing the gift tax rules

Beginning in 2018, you can gift up to $15,000 (or $30,000 if you’re married) to a person in a year without IRS interfering with your transaction. If you are gifting more than that amount, you need to file a gift tax return. That doesn’t mean that you have to pay a tax on the gift. It means that $15,000 is eligible for lifetime exclusion. This is the amount you can gift away during your lifetime without incurring a gift tax. The total lifetime tax exclusion for gifts is $11.2 million per individual; so, gift tax rules are not much of a concern for most people.

#2 Convert your retirement savings into alife insurance policy

Convert your retirement savings into an income tax-free gift (life insurance) for your spouse, children or grandkids.Here’s how it works:

You can withdraw the RMDs from your IRA. Pay the tax applied on distributions. The balance amount, you can use to pay the premiums on a life insurance policy. By doing so, you are turning a 100% taxable investment into 100% tax-free.

If you gift your IRA or a 401(k) to your loved ones, other than your spouse, they have to take distributions the next year, whether they want it or not. And if they are withdrawing, then they have to pay taxes on the withdrawals. The best part of life insurance is that the beneficiary doesn’t need to pay taxes on the amount they receive. It is a true gift.

#3 Can you gift money from an ira without paying taxes.

Let your children inherit your IRA. While you are alive, you have no tax benefit to gifting an IRA. Rather, consider passing it on as part of your estate plan. If your kids inherit your traditional IRA, you get to avoid the taxes while they benefit from the funds you have saved for years. However, they need to pay income tax on the amount they withdraw. A Roth may be a great way to leave your money to your kids without them paying the tax because you have already paid it.

Tax rules involved in gifting your retirement money to your family or loved ones can be confusing. If you need more information, call (866) 639-0066 for expert guidance.

Rick Pendykoski is the owner of Self Directed Retirement Plans LLC, a retirement planning company based in Goodyear, AZ. He has over three decades of experience working with investments and retirement planning, and over the last ten years has turned his focus to self-directed ira accounts and alternative investments. If you need help and guidance with traditional or alternative investments, call him today (866) 639-0066.

After being in the workforce for decades, retirement finally brings you the freedom to spend your time your way. And if you are fortunate enough to be physically healthy, financially sound, and have little-to-no custodian responsibilities, then there are endless possibilities for you to make the most of your retirement.

But if your retirement plans rely on your IRA income, now is the time to test things out. Can you live frugally and still enjoy your retirement? You won’t really know until you automate a transfer to your savings account to mimic the income you would be receiving from your 401(K) plan or other qualified IRA.

Here are 6 good things to do with your time during retirement to make it more meaningful and enjoyable:

1. Explore the World

Now that you don’t have to worry about pending work and leave applications being approved, take that much-awaited extended vacation. You can go on one-day trips, take a long cruise and travel to foreign lands, or simply set off on a whiskey tasting tour to Tennessee and get back! If you feel a little adventurous, you can raft your way to the Grand Canyon or head out for a hike and hit the red rocks in Southern Utah or simply go live in a whole new country.

2. Remodel Your Home for a Refreshing Vibe

Whether you’ve always desired a complete overhaul or simply want to upgrade a part of your home; now is the time to make all the repairs and replacements. You can use the required minimum distributions from your 401(k) plans to pay for your remodel or you can also consider earmarking your renovation dollars in a savings account.

3. Make Retired Friends with Similar Hobbies

Join a meet-up group of retired people who are geared to interests or leisure activities you like. It can be a reading club, a social network, or a group that organizes camps like fishing, swimming, hiking, snow skiing, surfing, or kayaking.

4. Rekindle the Important Relationships of Your Life

If you both are retiring around the same time, you are going to be spending ample of time together. Working on the relationships that are important to you now will help you keep things fresh and enjoyable. At home, you can trade responsibilities with your partner and plan outings that enrich your life. You can also make plans with close friends with whom you have strong bonds so that this transition becomes more fun and exciting.

5. Start a Sport You Enjoy or Join a Fitness Group

Join a sports league where you can regularly participate in sports like tennis, soccer, or bowling. Or you can commit to a new active lifestyle by joining a group that is devoted to living a fit and healthy life. Joining a group where everyone is dedicated to getting into their best shape and staying fit, will improve your quality of life and help keep aging related illnesses at bay.

6. Learn a New Language or Learn to Play an Instrument

Retirement brings you a lot of time to make foreign trips so learning a new language will serve you well during extended holidays. Learning a new foreign language will also help you keep your mind sharp.

You can also consider taking piano or guitar lessons as it will help you uncover a new talent and put you in the spotlight at all the family get-togethers and parties. You can also make the most of your newfound freedom by volunteering, teaching, taking up a part-time job, or starting your own business.

Whatever you choose to do during retirement, make sure you know all the smart withdrawal strategies so you avoid penalties and pitfalls. Safeguard your financial future by knowing what to do and what not to do with your 401(k) plans or any other types of IRAs. Before tapping your retirement reserve, call (866) 639-0066 for expert advice.

Rick Pendykoski is the owner of Self Directed Retirement Plans LLC, a retirement planning company based in Goodyear, AZ. He has over three decades of experience working with investments and retirement planning, and over the last ten years has turned his focus to self-directed ira accounts and alternative investments. If you need help and guidance with traditional or alternative investments, call him today (866) 639-0066.

Get Immediate Access to Our TOP RATED Retirement Videos

Learn all about self-directed IRAs and personal 401(k)s in these featured videos from our exclusive collection. Complete the form below to gain immediate access.