Emergencies aren’t exclusive or selective. They happen to everyone. It’s highly likely that you’ve faced events or obstacles in life that could be easily categorized as an emergency. These emergencies can catch you off guard and most often than not, have financial ramifications.

An emergency as simple as a car breakdown or as serious as a health issue can turn your life upside down. While we can’t predict when the next emergency will occur, we can definitely prepare for it by building emergency funds.

While an emergency fund doesn’t solve all your money problems, it’s the backbone of any strong personal financial plan. It’s a great way to get your finances sorted and headed in the right direction. In this article, we’ll look at what an emergency fund is, how much emergency fund you should have, including how to build an emergency fund and the best options to park your emergency fund.

What is an emergency fund?

An emergency fund is an amount of money that you set apart from your other savings for future mishaps and unexpected expenses. It is a financial safety net that you can easily and immediately accessible at the hour of crisis.

Having an emergency fund gives you the peace of mind to know that if something truly awful happens, you are in a position to deal with the emergency itself without having to worry about how you’re going to survive it financially.

Some situations that can be categorized as emergencies are:

Job loss

Car repairs

Home repairs

Death in the family

Unexpected hospital visits

That said, an emergency fund should only be used for true emergencies. It’s not a backup cash account that can be used for planned purchases and expenses, such as college education, vacations, car, house, and so on.

How much emergency fund should I have?

There is no simple one-size-fits-all answer to this question. Most financial experts recommend having an emergency fund of three and six months worth of living expenses. If your finances allow you, then you can consider expanding your emergency savings.

Below given are a few situations where having more in your emergency fund can help:

If your income isn’t steady

During a recession

If you’re in an industry where layoffs are common

If you’re retired and a major chunk of your money is locked in stocks and bond investments

Where to keep the emergency fund?

You should keep your emergency funds where they are easily and quickly accessible to cover the unexpected expenses. Although you want quick access to money, you wouldn’t want your emergency fund to be too convenient to reach so that you are tempted to dip into these funds. It’s best to keep your emergency fund separate from your other bank accounts.

Here are some of the best options to park your emergency fund:

When choosing where to save your emergency fund, consider these 3 factors:

You should be able to immediately withdraw the money when you need it.

You should not attract any penalties for withdrawals.

The value of the amount invested should deliver excellent returns.

How to build your emergency fund?

Take the following steps to build your emergency fund:

Figure out how many months of expenses you need to save depending on your personal circumstances and risk factors.

When calculating monthly expenses, add up only the essential expenses you need to cover in case of an emergency. Leave out optional expenditures like travel and dining out.

Multiply your monthly expenses by the number of months you want to save.

Set up automatic deposits into your emergency savings account.

If you come across other money, such as side hustle income, tax refund, etc., deposit it in your emergency fund to reach your goal faster.

Summary

If you don’t have an emergency fund, start building it today. Cut your expenses, earn extra income and save “found” money to build your emergency fund as fast as you can. Need expert advice? Contact Self Directed Retirement Plans LLC

Rick Pendykoski is the owner of Self Directed Retirement Plans LLC, a retirement planning company based in Goodyear, AZ. He has over three decades of experience working with investments and retirement planning, and over the last ten years has turned his focus to self-directed ira accounts and alternative investments. If you need help and guidance with traditional or alternative investments, call him today (866) 639-0066.

Retirement planning is important if you want to retire comfortably and achieve your retirement goals. A key part of retirement planning is deciding between which retirement withdrawal strategies i.e. which is the best for you and how different factors affect your retirement savings.

This small guide on retirement distribution strategies is a help to make you choose the best withdrawal strategy and make the most out of your retirement income.

Retirement Income Sources

When you are in retirement, you are probably generating income through these common retirement income sources.

Pension

Social Security

401(k) plan or similar defined contribution accounts

Taxable investments

Individual retirement accounts (IRAs)

Employment or self-employment income

A health savings account (HSA)

An annuity

4 Factors That Affect Your Retirement Income

Before you choose a retirement withdrawal strategy, you need to consider the following factors that affect your retirement savings.

Social Security and pension benefits: You can take your Social Security benefits when you reach the full retirement age of 67 years. You can also take early benefits at age 62. But, if you take the benefits early, your monthly benefits are reduced. If you wait until the full retirement age, you’ll receive 100% of your monthly benefit. Moreover, if you delay taking your benefits past your full retirement age, you’ll receive increased benefits until age 70, after which the benefits stop increasing, even if you decide not to take them. If you’re eligible for a pension, figure out what type of survivorship option to select, when to start taking the pension, and how to withhold taxes. Additionally, decide on how to maximize your pension payouts – lump sum or annuities – as they both affect your retirement income.

Portfolio diversification: You should have a variety of income sources in your portfolio if you want to get the most out of your funds. Invest in interest-bearing assets and also have non-correlated investments, such as stocks and bonds. While creating your portfolio, consider your age when investing. You do not want to rely solely on stocks and gravely hurt your financial situation when there is a drop in the market.

Life expectancy: The Social Security Administration stated that the average life expectancy for a woman who is 65 years old today is 86.5 years and 84 years for a man. And, 1 out of 7 people will live to be age 95. If you are retiring at age 65, you need to make your retirement saving last for another 20 or 30 years. Your living expenses and taxes are not the only costs you need to consider. Healthcare costs are a major expense and they increase as you age.

Taxes: Many retirees owe taxes on their Social Security benefits, pension or annuity payments, and/or even on the money they withdraw from their retirement savings accounts (traditional 401(k) or IRA). When you’re budgeting for retirement, determine how much you will pay annually in taxes so that you know how much money is available to you when you retire.

Retirement Withdrawal Rules

There are different rules for different types of retirement savings account regarding withdrawal age and Required Minim Distributions (RMDs). For example, withdrawals from 401(k)s are treated very differently than those from Traditional and Roth IRAs.

When can I start withdrawing money from my IRA?

You can withdraw money from your IRA (penalty-free) when you turn 59 ½ years old. Early withdrawals are also allowed, but it will cost you a 10% early withdrawal penalty unless you qualify for an exception.

When do I have to start making withdrawals from my IRA?

You need to start withdrawing from your traditional IRA when you reach age 72 ½ unless you’re still employed. The amount you need to withdraw is called required minimum distribution (RMD).

You can withdraw more than the RMD, but these withdrawals made from a traditional IRA are taxable. However, if you don’t take the RMDs, you are liable to pay 50% excise tax.

However, Roth IRAs don’t require withdrawals until the account holder dies. Since contributions in your Roth IRA are made with after-tax dollars, your money grows tax-free, and your withdrawals in retirement aren’t taxed.

When can I start withdrawing money from my 401(k)?

You can start withdrawing penalty-free money from your 401(k) when you turn 59 ½. You can also withdraw early, but you will have to pay an additional 10% early withdrawal tax penalty unless you are eligible for an exception.

When do I have to start making withdrawals from my 401(k)?

When you turn 72 ½, you have to take RMDs from your 401(k), unless you are still working. Your RMDs are taxed as ordinary income.

Retirement Account

Age at which you can start withdrawing money Tax-free

Age at which you need to start taking money according to required minimum distribution (RMD)

Traditional IRA

59 ½ years old

72 ½ years old unless you’re still employed

Roth IRA

59 ½ years old

–

401(k)

59 ½ years old

72 ½ years old< unless you’re still employed

*If you take widrals before you are 59 ½ years old then you need to pay an additional 10% early withdrawal tax penalty

Retirement Withdrawal Strategies

Whether you’re invested in an IRA, a 401(k) or another type of plan, you need to design a withdrawal strategy to provide the income you need to fund your retirement. Consider these 5 withdrawal strategies:

The 4% rule withdrawal strategy

Fixed-dollar withdrawal Strategy

Fixed-percentage withdrawal Strategy

Systematic withdrawal Strategy

Buckets withdrawal strategy

The 4% rule withdrawal strategy

This is the most common of all retirement withdrawal strategies. In the 4% rule, you withdraw 4% of your retirement savings in the first year of your retirement. In the next few years, you continue to withdraw 4%, making sure you scale up appropriately to factor in inflation.

This simple method is considered safe as it keeps your buying power at pace with inflation. However, with rising market volatility and increased interest rate, you are at risk of running out of money. Also, this rule doesn’t provide the flexibility to adjust your withdrawals based on the performance of your investments.

Bucket withdrawal strategy

The bucket strategy comprises splitting your savings based on your expenses into different accounts. For example, in your savings account (first bucket), you keep your living expenses for a year and a few months’ worths of the emergency fund. In fixed-income investments (second bucket), you can keep a couple of years’ worth of living expenses. The rest of your savings is retained in your retirement accounts or investment accounts (third bucket).

The best part of this approach is that you use your savings account for your living expenses, and refill this bucket with money from the other two buckets. To refill, you either sell the stocks when the market is up or sell you fixed income securities when they have performed well. If both stocks and bonds are not performing, you continue to draw from your savings.

This withdrawal approach allows you to have more control over your investments and help your account balance grow over time. but, this is a time-consuming process, and you may need to use another method to figure out how much you can afford to spend each year.

Fixed-dollar withdrawal strategy

In the fixed-dollar strategy, you withdraw a fixed amount over a specific period of time. You determine how much you need to withdraw each year and then reassess that amount every few years. The withdrawal amount can be increased or decreased to match the value of your investment portfolio. Although this approach allows you to determine the amount to withdraw based on your budget in your first year of retirement, it has substantial downsides. Firstly, if you don’t increase your withdrawal amount, your buying power will reduce because of inflation. And if you increase your fixed-dollar amount, you are at risk of running out of money too soon in retirement.

Fixed-percentage withdrawal strategy

In this type of withdrawal strategy, you withdraw a fixed percentage of your portfolio annually. The amount you withdraw will vary as the value of your portfolio rises or falls.

This withdrawal approach naturally adjusts your withdrawals in response to market fluctuations. However, if your withdrawal percentage is high, you risk being out of money very soon. Also, since your retirement income changes from year to year, you may find it difficult to make financial plans.

Systematic withdrawal strategy

In this withdrawal strategy, you keep the principal intact and only withdraw dividends or interest generated by the investments in your portfolio.

With this approach, you cannot run out of money in your retirement account. Unfortunately, your nest egg needs to be big enough to provide enough income to last for as long as you live. Since the income varies every year, depending on market performance, you might find it difficult to create a financial plan; moreover, if your investments don’t grow with the rise of inflation, your buying power can drop drastically.

Retirement Withdrawal Strategies At a Glance

Retirement Withdrawal Strategy

How It Works

The 4% rule withdrawal strategy

Withdraw 4% of your account balance in the first year of retirement, then adjust the amount upward after a few years to keep pace with inflation.

Bucket withdrawal strategy

Distribute the retirement assets into different accounts: some in a savings account, some in fixed-income securities, and some in equities. Draw money from the savings account and refill it with money from the other two accounts when they are performing well.

Fixed-dollar withdrawal strategy

Withdraw the same amount each year

Fixed-percentage withdrawal strategy

Withdraw the same percentage of your account balance each year

Systematic withdrawal strategy

Withdraw only income from your investments (interest and dividends), keeping the principal invested.

The right retirement withdrawal strategy for you will depend on how much retirement savings you have, how worried are you about outliving your money, and whether you’re considering extreme early retirement. These withdrawal strategies may not be a one-size-fits-all solution. You can consider a mix and match to come up with an optimal retirement withdrawal strategy unique for your circumstances.

Rick Pendykoski is the owner of Self Directed Retirement Plans LLC, a retirement planning company based in Goodyear, AZ. He has over three decades of experience working with investments and retirement planning, and over the last ten years has turned his focus to self-directed ira accounts and alternative investments. If you need help and guidance with traditional or alternative investments, call him today (866) 639-0066.

When you are young, retirement planning is something that you can easily put off to worry about later. After all, everything sorts itself out in the end. But, if it doesn’t, what’s your plan?

If you don’t have a plan, you will put yourself and your family in a less than ideal situation. If you have envisioned your dream retirement, you need to carefully plan your finances to realize those dreams.

A 401(k) plan is a common investment vehicle that Americans use to save for retirement. It is an employer-sponsored plan that allows you to make tax-sheltered contributions ($22,500 / $30,000 per year in 2023) to help maximize your retirement fund value.

According to a study sponsored by Personal Capital and conducted by ORC International, almost 37% of pre-retirees have no money saved for retirement. Nearly 63% of Americans participate in an employer-sponsored retirement plan, and just 21% of them max it out.

Let’s find out the 401(k) savings potential by age and what should be your retirement goals.

Average 401(k) Balance By Age

The below numbers show how the 401(k) average and median balance increase with age until the participant starts withdrawing money from it in retirement. These numbers may seem high to some people, especially if you are older and had started your retirement savings when the contribution limit was much lower. But, these numbers can be used as a guide for creating your retirement goals at every age.

Age

Average Account Balance

Median Account Balance

Under 25

$5,236

$1,948

25-34

$30,017

$11,037

35-44

$76,354

$28,318

45-54

$142,069

$48,301

55-64

$207,847

$71,168

65+

$232,710

$70,620

Group 1: Ages Under 25

Average 401(k) balance

Contribution rate (% of income)

Median 401(k) balance

$5,236

8.1%

$1,948

The participants in this age group are new to working and also new to retirement savings. At this young age, it is important to prioritize contributing to your workplace, especially if your employer matches a portion of your contributions.

Retirement Savings Goal: By the time you are age 24, you should have less than that amount saved and half have more.

Group 2: Ages 25-34

Average 401(k) balance

Contribution rate (% of income)

Median 401(k) balance

$30,017

10.7%

$11,037

At this point, the participant’s balances increase roughly fourfold. People of this age group spend more time in the workforce and are more likely to change jobs without rolling over or combining their retirement accounts. Therefore, they tend to hold more than one 401(k).

Retirement Savings Goal: By the time you are 34, you should have three times your annual salary banked into your 401(k) account.

Group 3: Ages 35-44

Average 401(k) balance

Contribution rate (% of income)

Median 401(k) balance

$76,354

11.1%

$28,318

In this age group, both the average balance and the median balance take a huge leap to become more than double. The reason could be that this age group is at its peak earning years. According to compensation research company Payscale, women tend to peak at age 39 and men at age 48.

Retirement Savings Goal: By age 44, you should have a 401(k) balance of at least six times your annual salary.

Group 4: Ages 45-54

Average 401(k) balance

Contribution rate (% of income)

Median 401(k) balance

$142,069

11.7%

$48,301

This age group is allowed to make catch-up contributions. Participants age 54 and older can contribute an extra $7,500 a year in 2023. This is helpful for those who have been falling behind in saving for retirement.

Retirement Savings Goal: By the time you reach age 54, your 401(k) balance should be eight times your salary.

Group 5: Ages 55-64

Average 401(k) balance

Contribution rate (% of income)

Median 401(k) balance

$207,874

12.9%

$71,168

This age group shows slow growth. This could be because the latter half of this group is already withdrawing from their 401(k). As people begin to tap into their accounts, the 401(k) balances begin to fall.

At age 59½, the IRS allows 401(k) distributions, although many people do not retire at that age.

According to Gallup, the average retirement age for Americans reported is 61 years, and the Social Security full retirement age for people is 67 years.

Retirement Savings Goal: By age 67, the account balance should be 10 times your annual salary. For example, if you are 67 years old earning $70,000 per year, you should have $700,000 saved in your retirement account.

Group 6: Ages 65+

Average 401(k) balance

Contribution rate (% of income)

Median 401(k) balance

$232,710

12.7%

$70,620

As of January 2020, the Further Consolidated Appropriations Act lifted the age limit that prevented participants 70½ or older from making contributions to traditional IRAs. This is an additional retirement saving option for those who are currently working or running their own business.

Note: There’s also the tried-and-true, 80% rule: This rule is to save as much as 80% of your pre-retirement salary. So, if you are earning $75,000 annually, and if you want to keep the same standard of living in retirement, you would need roughly $60,000 a year.

Bottom Line

The average 401(k) balances by age mentioned above is a fairly arbitrary benchmark. It can help you analyze your own situation. But, it’s also limited to people who have a 401(k) and many workers don’t.

It is worth mentioning that you should not put all your retirement funds into a 401(k) basket. Spread your retirement money into other retirement accounts such as an IRA after you have earned your employer match in your 401(k).

Do you have enough in your 401(k) to retire when you want? Need a more personalized recommendation for how much you should save, and how much you’ll need in retirement? Talk to an expert at Self Directed Retirment Plans LLC as soon as possible.

Rick Pendykoski is the owner of Self Directed Retirement Plans LLC, a retirement planning company based in Goodyear, AZ. He has over three decades of experience working with investments and retirement planning, and over the last ten years has turned his focus to self-directed ira accounts and alternative investments. If you need help and guidance with traditional or alternative investments, call him today (866) 639-0066.

A required minimum distribution (RMD) is the minimum amount of money you must withdraw from your tax-advantaged retirement accounts each year once you turn 72 years of age.

Age for RMD

Earlier, the RMD age was 70½ years. But, the retirement age for withdrawing RMDs changed in 2020. You now have to withdraw RMD by April 1 following the year you reach age 72.

On March 27, 2020, the CARES Act, signed by President Donald Trump, suspended RMDs from retirement accounts for 2020. However, the exemption is not extended in 2021. So, people who are already 72 or above will have to start or resume taking RMDs by year-end or get penalized.

By making it mandatory for you to begin taking RMDs after you reach 72, the government ensures that it receives the tax revenue it’s been waiting for and makes sure that taxpayers aren’t accumulating tax-free wealth indefinitely.

The Internal Revenue Service (IRS) has a worksheet prepared for taxpayers to calculate the RMD amount. Usually, the plan administrator or the account custodian calculates the RMD amount and report it to the IRS.

To calculate your RMD, all you have to do is divide your tax-deferred retirement account balance as of December 31 of last year by your life expectancy factor from the IRS Uniform Lifetime Table.

IRA Required Minimum Distribution Table

Age of retiree

Distribution period (in years)

72

27.4

73

26.5

74

25.5

75

24.6

76

23.7

77

22.9

78

22.0

79

21.1

80

20.2

81

19.4

82

18.5

83

17.7

84

16.8

85

16.0

86

15.2

87

14.4

88

13.7

89

12.9

90

12.2

91

11.5

92

10.8

93

10.1

94

9.5

95

8.9

96

8.4

97

7.8

98

7.3

99

6.8

100

6.4

101

6.0

102

5.6

103

5.2

104

4.9

105

4.6

106

4.3

107

4.1

108

3.9

109

3.7

110

3.5

111

3.4

112

3.3

113

3.1

114

3.0

115

2.9

116

2.8

117

2.7

118

2.5

119

2.3

120 and older

2.0

How To Calculate RMD

Required Minimum Distributions (RMDs) are calculated based on an individual’s age and the balance of their retirement account, typically using IRS-approved life expectancy tables to determine the annual distribution amount.

The RMD calculation is a 3-step process:

Note down the balance of your account as of December 31 of the previous year.

Find your life expectancy factor on the IRS Uniform Lifetime Table. Look for the factor that is corresponding to your age on the birthday of the current year. This factor number for most people is between 27.4 and 1.9. As your age increases, the factor number decreases.

To find the RMD, divide your account balance by the factor number.

Required Minimum Distribution (RMD): An Example

Steve is 74 yrs old. It’s nearing April, and on October 1, Steve will be 75. His IRA is worth $275,000. As of December 31 of the previous year, his account balance was $225,000. The distribution factor from the relevant IRS table for age 75 is 22.9. So, let’s calculate Steve’s RMD.

RMD = $225,000 ÷ 22.9 = $9835.32

So, Steve needs to withdraw at least $9835.32.

If Steve has multiple IRAs, he must calculate RMD separately for each account. Depending on the types of accounts Steve has, he may have to take RMDs separately from each account instead of taking all RMDs from one account.

The IRS has different calculation tables for different situations. For example, there will be a different calculation table if the account holder’s spouse is the account’s only beneficiary and is more than 10 years younger than the account holder. For married couples with age differences, the IRS has a separate table called the Joint Life Expectancy Table. In this table, your life expectancy factor is based on both spouse’s ages.

For example, let’s say Janet is 75 and her husband Brad is age 64. Janet’s account balance was $100,000 as of December 31 of last year. According to the IRS Joint Life Expectancy Table, their factor is 23.6.

When the account balance is divided by the life expectancy factor, Janet’s RMD is $4,237.29.

RMDs and Inherited IRAs: Special Case

If you inherit an IRA, you may also be subject to RMDs. After the account owner’s death, the nature of the relationship you had with the deceased will decide the type of RMD you’ll face. For example, RMD rules may vary depending on whether you are a minor child, surviving spouse, or a disabled individual.

If you inherit an IRA from an account holder;

Who died prior to January 1, 2020, you’ll use your IRS Single Life Table to calculate your RMD

Who died after December 31, 2019, you’ll need to follow the RMD rules established by the SECURE Act, which clearly distinguishes between designated beneficiaries, eligible designated beneficiaries, and non-designated beneficiaries. Depending on which category you belong to, the calculation and timeframe of your RMD may vary.

FAQs related to Required Minimum Distributions

Who calculates the amount of the RMD?

Usually, the IRA custodian or retirement plan administrator calculates the RMD and report it to the IRS. But the responsibility lies with the retirement account holder.

What happens if a person does not take an RMD by the required deadline?

If an account owner does not withdraw the RMD, fails to withdraw by the required deadline or doesn’t withdraw the full RMD amount, the RMD amount that’s not withdrawn is taxed at 50%.

Can an account owner withdraw more than the RMD?

Yes. The account holder can take more than the RMD without penalty. However, the withdrawal amount will be taxed the same way the RMD is taxed.

Can a distribution in excess of the RMD for one year be applied to the RMD for a future year?

No. An excess of the RMD for one year cannot be applied to a future year.

Can the penalty for not taking the full RMD to be waived?

Yes. The penalty can be waived if the account holder is able to establish that the withdrawal shortfall was due to a reasonable error and that steps were taken to rectify the error.

Are Roth IRAs subject to RMDs?

Roth IRAs are not subject to RMDs. If you don’t need the money, you can let the money in the account grow untouched and tax-free.

Can RMD amounts be rolled over into another tax-deferred account?

The IRS rules prohibit investing your RMD into another tax-advantaged retirement account. However, you can consider converting the remaining portion of your traditional IRA assets to a Roth IRA, but this may mean paying more taxes.

At What Age RMD Stop?

RMDs (Required Minimum Distributions) typically stop at age 72, based on current IRS regulations. This age was increased from 70½ through the Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in 2019.

Rick Pendykoski is the owner of Self Directed Retirement Plans LLC, a retirement planning company based in Goodyear, AZ. He has over three decades of experience working with investments and retirement planning, and over the last ten years has turned his focus to self-directed ira accounts and alternative investments. If you need help and guidance with traditional or alternative investments, call him today (866) 639-0066.

A 401(k) plan allows you to put a certain amount of your salary into a retirement account in which your investment gains are tax-free until you start withdrawing from it. You also get to earn free income when your employer matches the amount of money you put into your retirement plan, up to a certain limit.

However, when you need money due to an unexpected large expense or an emergency, you might wonder – can I cash out my 401(k)? In this article, we’ll look at the eligibility, consequences and the process to cash out your 401(k) early.

Eligibility to cash out your 401(k)

So , when can you withdraw from 401k? You need to meet certain criteria before you can cash out your 401(k). Have a look at these prerequisites to avoid making costly mistakes.

If you’re still working for the employer that sponsors your 401(k) plan,you are not eligible to cash in your plan and savings. However, you can check whether your plan allows you to take a 401(k) loan or hardship withdrawals to get you out of the situation you are in.

If you’re no longer employed with the company that sponsored your 401(k) plan,you can access the funds. You can either consider to cash out your 401(k) or roll over the balance into an IRA or a private self-directed 401 k plan.

If you wish to cash out all or part of a 401(k) fund without being penalized,then you need to be either:

of age 59½ or above or

Disabled, or

Undergoing some sort of financial “hardship”(if your plan allows)

Consequences of cashing out a 401(k) or 401(k) early withdrawal

If you choose to withdraw funds early, you should prepare yourself for these consequences:

A 20% of a 401(k) early withdrawal will be withheld for taxes.If you withdraw $10,000 from your 401(k) at age 45, you may get only about $8,000. You might get this money back as a tax refund if the withholding exceeds your actual tax liability.

You’ll be charged a 401(k) early withdrawal penalty of 10% if you withdraw before age 59½. This means you are giving away an additional $1,000 of that $10,000 withdrawal to the government. After taxes and penalty, you could be taking home just $7,000 from your original amount of $10,000. Here is a detailed post on what will happen if you withdraw from your 401(k) before 59½ and after that.

You’ll have less money for your future.Cashing out 401(k) early means you’ll have less money to use when you retire. This can severely disrupt your entire retirement plan.

You’ll receive no credit protection.Funds in 401(k) plans are protected. In case of bankruptcy, your creditors cannot seize your funds. When you withdraw money from your 401(k), you lose this protection, which may make you vulnerable to hidden expenses in the long run.

Are you still contemplating taking a 401(k) early withdrawal or cashing out a 401(k)?

After knowing the consequences of early withdrawal of funds from your 410(k), if you are still considering cashing it out, then do the following:

See if you are eligible for a hardship withdrawal

Check whether you qualify for an exception to the 10% tax penalty

Follow these three steps to withdraw money early from your 401(k):

Check with the HR department to find out whether you can withdraw funds early. If yes, then find out whether you are eligible for it.

Get in touch with your 401(k) plan provider. Ask for information, and submit the required paperwork to cash out your plan.

Obtain the required signatures from your HR representatives or plan administrators at your former employer as an acknowledgement that you have filed the documentation to execute the process of cashing out your 401(k) early and is authorized to so.

How long does it take to receive money after you cash out a 401(k)?

You may have to wait for several weeks until you receive your funds. A 401(k) plan is a highly regulated retirement account subject to strict governance. Therefore, it may take a significant amount of time for the funds to be released.

Some plans may have rules that restrict them from giving out funds more than once a quarter or year. If your plan follows this rule, the time horizon can be extended to 30 – 90 days or more.

If you are contemplating cashing out your 401(k), but are concerned about its implications, be sure to consult a financial expert.

Rick Pendykoski is the owner of Self Directed Retirement Plans LLC, a retirement planning company based in Goodyear, AZ. He has over three decades of experience working with investments and retirement planning, and over the last ten years has turned his focus to self-directed ira accounts and alternative investments. If you need help and guidance with traditional or alternative investments, call him today (866) 639-0066.

Which is a better strategy for growing your wealth? Investing in real estate or stocks? Or a bit of both like most Americans do? The answer isn’t simple. However, understanding each type of investment will enable you to choose the best strategy to grow your money and create financial security.

Both real estate and stocks have their own set of pros and cons. Remember, many investors invest in both. If you like the idea of investing in real estate, 401(k) real estate investment might be worth a second look.

Let’s take a look at how real estate and stocks stack up against each other.

Real Estate vs Stocks

Returns

Real Estate: You are buying physical property, a piece of land, apartment, home, etc. If your property is vacant, it costs you money in terms of taxes and maintenance. But if your property is on rent, it generates rental income which you can spend on taxes and maintenance, and the rest can be considered as profit.

Stocks: When you invest in stocks, you buy the shares of a company. It’s like owning a small percentage of the company. As the company grows, the value of your shares grows too. Money is made in the stock market by buying low and selling high.

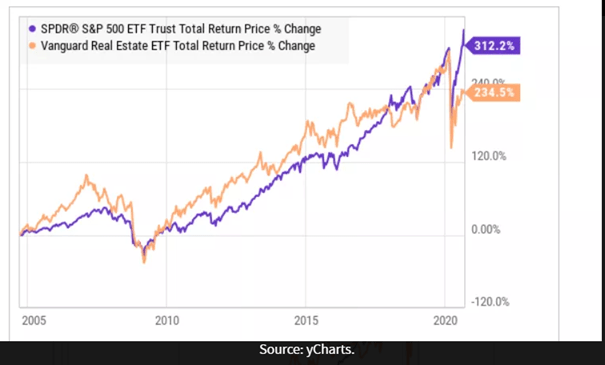

The returns of both these investments cannot be practically compared because the factors that affect values, prices and returns are very distinct. However, if we compare the total returns of the SPDR S&P 500 ETF (SPY) and the Vanguard Real Estate ETF Total Return (VNQ) over the last 20 years, we can get a fair idea of how they perform

The chart above indicates that both real estate and stocks take big hits during economic recessions. Notice the drop that occurred during the great recession (2008) and COVID-19 (2020).

The chart above indicates that both real estate and stocks take big hits during economic recessions. Notice the drop that occurred during the great recession (2008) and COVID-19 (2020).

Risks

Real Estate: When it comes to real estate, the most important risk is investing in it without doing thorough research. Also, you cannot easily liquidate your real estate when you are in a bind. If you own rental properties, the risks usually involve handling repairs or managing rentals.

Stocks: The value of the stocks is extremely volatile, and the prices can go up and down due to market fluctuations. The stock market involves economic, market and inflationary risks. If you have an undiversified investment portfolio, you attract greater risks.

Pros and Cons

Real Estate

Pros

Easy to understand: While the process of investing in real estate is complicated, the basic rules are simple – buy, maintain/manage, and resell at a higher price.

Tax advantages: Real estate investors can take advantage of substantial tax benefits in terms of tax reduction or tax breaks.

Hedge against investment: As the value of homes and rents typically increase with inflation, owning a real estate is generally considered a hedge against inflation.

Ease of Tranzactions: With growing digitalisation making transactions has become very easy with tools such as online rent payment and affordable esignature service the hassle of online paperwork is reduced making the transactions fast and smooth

Cons

More work than buying stocks: While the process of purchasing real estate is easy to understand, it demands more hard work.

ROI isn’t guaranteed: Although the price of property rises over time, you could be at risk of selling the property at a loss; the great recession is a reminder of that.

Expensive and liquidity-challenged: Real estate is expensive and highly illiquid. Buying real estate requires a large amount of cash as an upfront investment. It has high transaction costs. Getting money through reselling the property is also difficult. Although an asset, it’s not easy to liquidate it.

Highly liquid: It’s easier to know the value of the stocks. And if you decide to act (buy or sell), you can do it almost instantly.

Easy to add to a tax-advantaged account: Your investment can go tax-deferred or tax-free if you purchase shares through an employer-sponsored retirement account like a 401(k) or through an IRA.

Fewer transaction fees: You need a brokerage account to buy and sell stocks. Most brokers offer no-transaction-fee or zero trading costs.

Easy to diversify: You can build a broad portfolio of industries and companies at a fraction of the cost and time of owning a diverse range of real estate.

Cons

More volatile: Stock prices are volatile. They move up and down faster than real estate prices. This volatility can be risky unless you have a plan.

Potential for emotion-driven investing: Majority of the stock selling and buying decisions are made when the market fluctuates. If emotion, and not the strategy is the trigger, it becomes risky.

Selling stocks can trigger big taxes: Selling stocks may attract capital gains tax. Owning stocks for more than a year also attracts taxes, but at a lower rate. When your stock portfolio pays out any stock dividends, you may have to pay taxes.

Both real estate and stocks offer long-term financial gain, but they also come with potential risks. While choosing the best investment strategy to grow your wealth, the best way to hedge against the risks is to diversify as much as possible.

Rick Pendykoski is the owner of Self Directed Retirement Plans LLC, a retirement planning company based in Goodyear, AZ. He has over three decades of experience working with investments and retirement planning, and over the last ten years has turned his focus to self-directed ira accounts and alternative investments. If you need help and guidance with traditional or alternative investments, call him today (866) 639-0066.

Get Immediate Access to Our TOP RATED Retirement Videos

Learn all about self-directed IRAs and personal 401(k)s in these featured videos from our exclusive collection. Complete the form below to gain immediate access.