Key Takeaways

- Controlled group rules decide whether multiple businesses are treated as one employer for Solo 401(k) purposes, which directly impacts eligibility and compliance.

- A Solo 401(k) is only allowed when none of the businesses in the controlled group employ full-time workers (other than a spouse). One full-time employee in any entity disqualifies the entire group from using a Solo 401(k).

- All controlled group companies must follow the same retirement plan structure, meaning owners may need a standard 401(k) or Safe Harbor 401(k) if workers exist in any connected business.

- Contribution limits apply across all controlled group businesses combined. It prevents owners from using multiple entities to increase annual Solo 401(k) contributions.

If you own more than one business, you may wonder whether you can still use a Solo 401(k) plan. The answer depends on whether your businesses are treated as a controlled group under IRS rules. These rules decide if your companies must be viewed as one employer for retirement plan purposes.

This guide breaks down what a controlled group Solo 401(k) plan is, why it matters, and how to stay compliant so you can protect your plan and avoid IRS issues.

What Is a Controlled Group?

A controlled group exists when the IRS determines that multiple businesses are effectively under the same ownership or control. When companies fall into this category, the IRS treats them as one employer for retirement plan rules. This matters because if any business in the group employs full-time workers, all companies in the group lose Solo 401(k) eligibility.

Controlled groups can take any form, such as sole proprietorships, partnerships, S-Corporations, C-Corporations, LLCs, and tax-exempt organizations. The controlled group rules apply not only to corporations but also to all forms of businesses, including sole proprietorships, partnerships, and limited liability companies.

When companies fall into this category, the IRS treats them as one entity for retirement plan rules if there is common control or overlapping ownership. All controlled group members—meaning all companies that are considered part of the group for compliance purposes—must be included in coverage testing and plan considerations. This matters because if any business in the group employs full-time workers, all companies in the group lose Solo 401(k) eligibility.

The IRS determines a controlled group by examining common control and applying controlled group purposes, which involve specific ownership and attribution rules. Determining ownership includes reviewing direct ownership and ownership interest in each business, whether through stock ownership for corporations or capital/profit interest for partnerships. The process also considers stock attribution rules under IRC §318, which govern how ownership interests are generally attributed among family members. Under IRC §318, an individual is considered to own the stock owned directly or indirectly by their spouse, children, grandchildren, and parents. Family members are the most common source of attributed ownership for small business owners.

There are several types of controlled groups: parent subsidiary group (where one company owns at least 80% of another), brother-sister group (where the same five or fewer individuals, estates, or trusts own at least 80% of two or more companies), and combined group (a combination of parent-subsidiary and brother-sister relationships). Wholly owned entities are also included in these rules. Two companies or more than one company under common control may be considered a controlled group, even if they are not corporations.

Ownership for controlled group purposes is generally defined in terms of stock ownership for corporations or capital/profit interest for partnerships. Stock ownership and the application of stock attribution rules are critical in determining whether businesses are part of a controlled group.

Types of Controlled Groups

-

Parent-Subsidiary Controlled Group

This happens when one business owns 50% or more of another company.

-

Brother-Sister Controlled Group

This involves two or more businesses owned by the same person or group of people, meeting specific ownership and control tests:

- The same five or fewer individuals own 50% or more of each business.

- They have “effective control,” meaning identical ownership of more than 50%.

-

Combined Controlled Group

A mix of the above types is a combined controlled group. For instance, you own more than 50% of Company A, Company A owns 50% of Company B, and you also own a portion of Company C.

-

Family Attribution Rules

The IRS may “attribute” ownership among family members, including spouses, parents, and minor children. If your spouse owns 100% of a company, the IRS may treat you as owning it too.

What is the Impact of a Controlled Group on a Solo 401(k)?

If your businesses fall under a controlled group, the IRS treats them as a single employer for retirement plan purposes. The main impacts include:

- Solo 401(k) Eligibility Changes: The plan is no longer allowed if any company in the group has a full-time employee.

- Shift to a Standard 401(k): You may need a plan that covers all eligible employees across every connected business.

- Combined Contribution Limits: Your total compensation from all controlled group businesses is used to calculate a single annual contribution limit.

- Unified Plan Oversight: All companies are expected to follow the same plan structure to avoid compliance issues.

In short, controlled group status can eliminate Solo 401(k) eligibility and increase administrative requirements.

What are the Key IRS Rules for Controlled Group Compliance?

The IRS enforces controlled group rules to ensure business owners do not use multiple entities to bypass employee coverage requirements. These rules determine when companies must be treated as one employer:

-

Common Ownership and Control Tests Apply

The IRS evaluates ownership percentages, voting control, and family attribution to determine whether businesses are connected.

-

Employees Must Be Counted Collectively

Any full-time employee in any entity must be included when determining retirement plan eligibility.

-

Family Attribution Can Create a Controlled Group

Spouses, minor children, and certain relatives may be treated as owners. Sometimes, linking companies unintentionally.

-

One Combined Contribution Limit

Since controlled group companies are treated as one employer, owners cannot use separate entities to inflate contributions.

-

A Single Plan Must Cover the Entire Group

If the structure requires a full 401(k) plan, it must universally apply to all eligible employees across all companies.

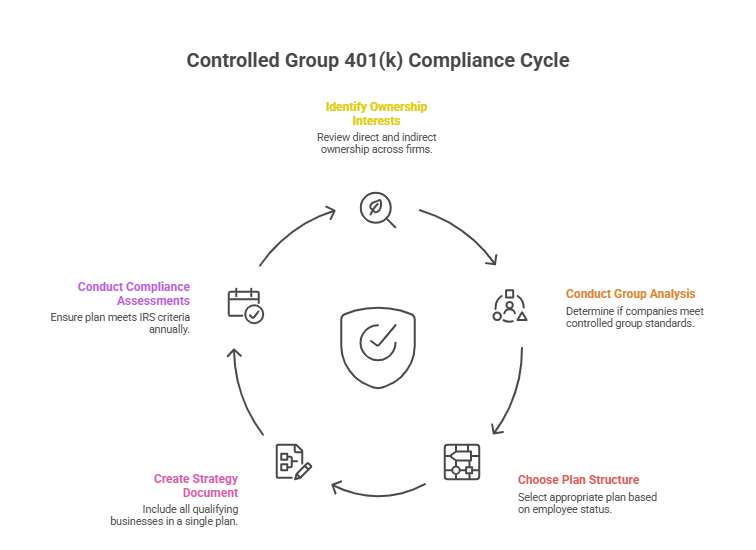

How Can You Set Up and Ensure Compliance for a Controlled Group Solo 401(k) Plan?

If your businesses form a controlled group, your retirement plan must be set up correctly to meet IRS requirements. This prevents plan disqualification and protects your tax-advantaged status.

Steps to Ensure Compliance

-

Identify all Ownership Interests

Review direct and indirect ownership across all firms you control. Add family attribution guidelines.

-

Conduct a Controlled Group Analysis

Use IRS guidelines or contact a specialist to determine whether your companies meet controlled group standards.

-

Choose the Proper Plan Structure

If there are no employees in any business, a solo 401(k) is still permitted. If any firm has employees, you may require a Traditional 401(k) or Safe Harbor 401(k) that insures everyone.

-

Create a Single, Cohesive Strategy Document

All qualifying businesses in the controlled group must be included under the same plan.

-

Conduct Yearly Compliance Assessments

Annual testing ensures your plan fulfills IRS coverage and non-discrimination criteria.

Pros and Cons of a Controlled Group 401(k)

A controlled group setup has its own benefits and challenges. Check them out here:

Pros:

-

Consistent Retirement Savings

You can streamline retirement planning across multiple businesses.

-

Increased Contribution Limits

Income from all controlled group businesses can support higher employer contributions.

-

Tax Benefits

Unified plans may offer additional deductions and smoother tax planning.

Cons:

-

Compliance Complexity

Solo 401(k) controlled group rules are detailed and require careful analysis.

-

Higher Administrative Costs

More businesses and employees usually mean more testing, documentation, and service fees.

-

Potential Loss of Solo 401(k) Status

If employees exist anywhere, Solo 401(k) eligibility ends.

Tax Implications of a Controlled Group Solo 401(k)

Navigating the tax implications of a controlled group Solo 401(k) can be challenging, especially when two or more businesses are involved. The IRS controlled group rules are designed to prevent business owners from sidestepping retirement plan requirements by splitting employees or ownership across multiple companies. When a controlled group exists—whether through a parent-subsidiary controlled group, a brother-sister controlled group, or an affiliated service group—the tax treatment of your Solo 401(k) plan changes significantly.

If your businesses are part of a controlled group, the IRS treats all companies as a single employer for retirement plan purposes. This means all eligible employees across the controlled group must be included in the 401(k) plan, and contributions must be made on their behalf. Failing to do so can result in the plan losing its tax-advantaged status and facing costly penalties.

The brother-sister controlled group rules, which apply when five or fewer individuals have a controlling interest in two or more businesses, can have a major impact on your tax benefits. Similarly, the parent-subsidiary controlled group rules come into play when one company owns at least 80% of another, affecting how contributions and coverage are calculated for tax purposes. In some cases, affiliated service group rules may also require you to aggregate employees from related companies, further complicating compliance and tax planning.

Understanding your ownership structure is crucial. Overlapping ownership, direct or indirect control, and family attribution rules can all trigger controlled group status. This impacts not only who must be covered by the retirement plan, but also how much you can contribute and deduct for tax purposes. If your plan fails coverage testing or excludes eligible employees, you risk losing valuable tax benefits and may face IRS penalties.

Given these complex rules, it’s essential to work closely with a tax professional and a knowledgeable retirement plan provider. They can help you determine your controlled group status, ensure all eligible employees are included, and structure your 401(k) plan to maximize tax benefits while staying compliant with IRS regulations.

Final Thoughts: Is a Controlled Group Solo 401(k) Plan Right for You?

A controlled group Solo 401(k) can work well if you own multiple companies with no full-time employees across any entity. But if you employ workers in any business, you need another type of retirement plan to stay compliant.

If you are unsure whether your companies form a controlled group, it’s best to get a professional review. The right structure can protect your tax benefits and keep your retirement plan in good standing.

Need help analyzing your ownership structure or setting up the right 401(k)?

Talk to a specialist at Self-Directed Retirement Plans LLC today.

FAQs

What happens if I disregard the rules of the controlled group?

Failure to comply can result in plan disqualification, IRS penalties, and taxable distributions. Before opening or making contributions to a Solo 401(k), it's critical to evaluate your ownership structure.

Are family-run companies inherently governed?

Family attribution rules may be applicable, but not always. For example, ownership can be divided between parents and minor children or between couples.

How can I find out if my companies belong to a controlled group?

You need to apply the IRS’s ownership and control tests or consult a certified tax advisor or ERISA attorney to do a full study.

Can I restructure my businesses to preserve my Solo 401(k)?

Yes, possibly. You may be able to separate your Solo 401(k)-eligible business from others through entity restructuring or ownership changes. But you should always do this with expert legal and tax assistance.

How do contributions work in a restricted group Solo 401(k)?

All contributions from all enterprises in the controlled group count against the yearly Solo 401(k) contribution limitations combined.

Can I modify a Solo 401(k) plan that was set up incorrectly?

Yes, but it demands corrective action, maybe including plan termination or conversion to a full 401(k). Seek expert help.

What if my spouse works for one of my businesses?

Spouses are allowed in Solo 401(k) plans. However, the plan can be invalidated if there are additional employees.